Assembly backs NYC pension gimmick in state budget

An amortization scheme with murky origins remains on the table as state budget negotiations begin in Albany

After popping out of the blue into Governor Kathy Hochul’s state budget amendments a few weeks ago, a proposed stretching-out of New York City’s pension funding schedule moved at least a half step closer to reality in Albany last week. Although it was among the Hochul provisions “intentionally omitted” from Senate Democrats’ amended one-house budget bills, the pension change was included without alteration in budget bills introduced by Assembly Democrats. The provision will be in the mix, at least initially, in budget negotiations between the governor and the Legislature between now and the April 1 state of the 2026 state fiscal year.

As described in this space on Feb. 21, the proposed recalculation of pension contributions is designed to generate a reduction of $11 billion in scheduled city payments over the next six years while pushing a net $18 billion increase in net projected tax-funded pension contributions into the early 2040s.1 This would result from re-setting the current unfunded liability amortization timetable in the city’s two largest pension funds, the New York City Employees’ Retirement System (NYCERS) and the New York City Teachers’ Retirement System (NYCTRS), along with those of the much smaller Board of Education Retirement System (BERS). The cost to future taxpayers would be higher because the unfunded liabilities would have to be compounded with interest across 12 more years than called for in the current schedule.

It isn’t just unusual but unprecedented for a statutory provision altering the mechanics of New York City’s pension plans to be included in a governor’s Executive Budget bill. The provision was inserted, the governor’s office said last month, “at the request of New York City”—on what happened to be the same day Hochul announced that, as the New York Times reported, she would “seek to impose strict new guardrails on his administration of New York City.”

The numbers

Like refinancing a loan that’s otherwise due to be paid off in a few years, the proposal embraced by the governor represents the kind of financial manipulation that state and local governments more typically consider only when they are desperate for cash. While New York City faces multibillion-dollar budget gaps over the next four years, it’s hardly that desperate. Mayor Eric Adams’ preliminary budget for FY 2026 projected that pension contributions will grow from $10 billion in FY 2025 to $11.8 billion in FY 2028, subsiding a bit to $11.3 billion in FY 2028—a net increase peaking at $1.8 billion, while salaries, wages, and fringe benefits are projected to rise during the same period by roughly $5 billion, accounting for a larger share of projected budget gaps.

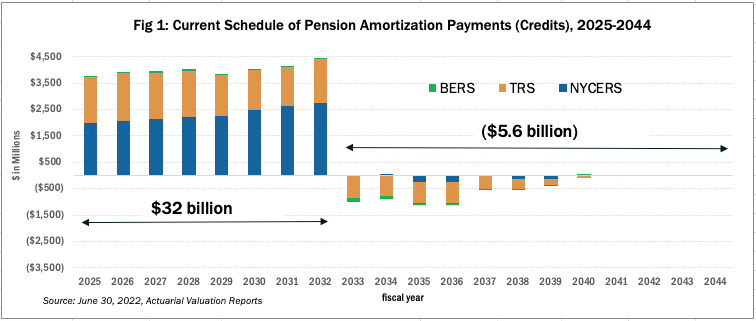

The current ERS, TRS, and BERS pension liability amortization schedules, enacted in 2013 and reflecting liabilities calculated as of 2010, are set to end in FY 2032. This will be followed by a sharp $4.5 billion drop in amortization-related contributions in 2033, followed by eight years of credited discounts stemming from the completion of the amortization schedule, as shown in Figure 1 below. The chart is derived from the most recent actuarial valuation reports for all three pension systems (which are incorporated in Adams’ preliminary financial plan numbers).

As shown in Figure 2, below, the proposed change would reduce contributions over the next six years—but lead to a sharp increase over current projections from 2033 into the 2040s. By that time, remaining unfunded pension liabilities dating back to 2010 will be more than 30 years old.

The official projections used to create these charts are strictly illustrative, assuming the pension funds hit their asset return target of 7 percent every year over the next 20 years, and assuming no further change in other actuarial assumptions or benefits levels. The actual totals will depend on asset returns as well as any changes to actuarial assumptions or benefit levels. However, the two charts convey an accurate picture of the crucial difference between the current schedule and the proposed change: roughly one-third of the remaining unfunded liability will be pushed forward another decade, from the early 2030s into the early 2040s, compounded by interest (also of 7 percent).

As noted here a few weeks ago, this scheme could never have surfaced without support from the two biggest unions whose members are covered by the pension plans, District Council 37 of AFSCME and the United Federation of Teachers (UFT), both of which have maintained public radio silence on the proposal. However, in a communique to retired union members last week2, UFT’s three retirement fund trustees let this much slip:

This proposed legislation is an attempt to protect our pension fund from market volatility by using an amortization process to extend the additional city contributions — which were set to end in 2033 — to 2045 …

While we understand the reasoning behind the legislation and we support the process, it requires a viable partner in City Hall that understands the intricacies of crafting pension legislation. We determined last Wednesday that we were no longer confident in the city's ability to be this partner. For this reason, on Thursday, we notified the city actuary that at this point in time we are not willing to support the legislation. Sadly, three days later, a group of people tried to use this issue to cause fear and anxiety among our members, especially our retirees. [emphasis added]

The message links to March 7 email from the UFT trio to City Actuary Marek Tyskiewicz, in which the union trustees cited unspecified “recent actions and comments by officials in the city’s Office of Management and Budget” as having “raised concerns about the city politicizing what should be a straightforward process designed to safeguard the city’s pensions.” Left unclear is exactly what “recent comments and actions” by OMB they were referring to (perhaps leaving Tyskiewicz puzzled as well).

The “last Wednesday” cited in the UFT message to retirees would have been March 6, coinciding with the City Council Finance Committee hearing on Adams’ preliminary budget. My cursory review of OMB Director Jacques Jiha’s appearance didn’t come across any mention of the pension change—but Comptroller (and mayoral candidate) Brad Lander did talk about it, under questioning from Councilmember Justin Brannan, chair of the Finance Committee.

Brannan:

The mayor has been lobbying in Albany to allow the city to refinance its unfunded accrual liability for three of the pension systems. This action would save the city in the short run but it would add additional costs in the long run. Council sees the merit of this proposal, but we don't think it's appropriate to move forward unilaterally without the support of the employees who fund and rely on the pension systems. What is your, the controller's office, opinion of this proposal? [emphasis added]

After a bit of meandering around the numbers, Lander acknowledged that “of course, if you stretch the [amortization] payments out longer, you can reduce what you would do between now and 2032” but that the change would also “cost the city… meaningfully additionally in the out years”—a point that bears repeating in all discussions of this thing.

After citing some of the projected differences in contribution numbers, Lander continued “it means substantially more dollars in the out years than you see savings in the next decade. And just to do that, kind of, ‘because’ [Lander injected air quotes at this point] does not make any sense.”

Then Lander spoke a quiet part out loud:

Now, you know, if there is a serious emergency created as a result of what happens in Washington and we see more specifically what that looks like, you might say, well, maybe we should take another look at that in the context of looking at long term retiree health benefit obligations as it becomes more clear what will happen with the resolution of the lawsuit and retiree health benefits, you might say. Let's bring that in and calibrate our long-term obligations more thoughtfully. So could there be potentially a responsible way of looking at this as part of a real fiscally responsible long-term plan? It's possible, and we would be glad to consider it. But the current proposal simply to take some money now and bill it to the future, we do not support. [emphasis added]

So, the city comptroller, the pension funds’ custodian and investment advisor, doesn’t like the idea of finagling with amortization schedules, but is open to changing his mind in an “emergency.” Brannan, meanwhile, indicated the Council is fine with the deal so long as the unions approve.

Keep that bit about retiree health benefits in mind when we turn to the subject of possible political motives near the end of this post.

Pension basics refreshers

In calculating how much money a pension fund must accumulate to make good on future retirement benefit promises, one of the most crucial variables is the interest rate used to calculate the net present value of current cash flows. The lower the discount rate, the more the city—i.e., always: city taxpayers—must contribute to pension funds every year to contribute to cover all future liabilities.

As recently as 2011, the city was still assuming annual returns of 8 percent rate, despite a decade of wild stock market volatility, and even though market rate bond yields at that point were sinking much lower. That’s when the Bloomberg administration and then-City Actuary, Robert North, agreed to support a state law reducing the discount rate to 7 percent. However, simply imposing the change all at once would have created an additional $20 $41 billion unfunded pension liability. To cushion the budget blow, the actuary came up with a plan to spread the cost of the transition across a 20-year amortization schedule, requiring extra payments to be made each year through FY 2032.

The latest ERS and TRS actuarial reports project that the current amortization periods will produce a one-year windfall of sorts, in the form of a roughly $5 billion net reduction in combined tax-funded ERS and TRS employer contributions in FY 2033.

Why bother?

So why finagle with pension contributions now? Start by considering the 2012-13 pension deal. The actuary wanted a lower discount rate, and OMB wanted to reduce projected contributions. A similar tradeoff may be at work here. The city actuary’s fiscal note, as attached to Hochul’s bill language, ends with this explanation of another, technical aspect of the change:

IMPACT ON ASSET SMOOTHING: This legislation modifies the approach used to smooth investment gains and losses. The current asset smoothing method phases in the recognition of investment gains and losses over a five- year period producing an Actuarial Value of Assets (AVA) used to determine the UAL [Unfunded Actuarial Liability] and related amortization payments that is different from the Market Value of Assets (MVA).

The proposed legislation would recognize the full investment gain or loss immediately with a five-year phase-in and five-year phase-out of the payments over a twenty-year period in total. This alternate method produces a contribution smoothing effect similar to the current method and eliminates the need to calculate an AVA different from the MVA. The smoothing corridor currently used to constrain the AVA within plus or minus twenty percent of the MVA becomes obsolete under this legislation.

Calculating the retirement systems’ funded status based on the market value of their assets—as opposed to a modified “actuarial” measure of asset value—provides for a more accurate and transparent calculation of asset values. However, the UFT trustees’ claim that this change would “protect our pension fund from market volatility” is a stretch. If anything, it might introduce more year-to-year volatility to the calculation of asset values, but coupled with the longer amortization period for liabilities, it should not add volatility to the required employer contribution amounts—i.e., what the taxpayers must come up with every year.

The shift to the unbounded MVA measure of “smoothed” assets is desirable from the actuary’s perspective. But if no change is made, the city is assured that pressure on contributions is going to decrease significantly starting with the end of the amortization period in seven years. As noted and depicted above, this proposal would stretch the unfunded liability further into the future. Think of it as, among other things, intergenerational inequity.

Pension plans should aim to maintain sufficient assets to cover at least 100 percent of liabilities. The three pension plans affected by this proposal aren’t there yet. As of their latest actuarial valuation reports (based on data as of the year ending June 30, 2022, which was a year of subpar investment gains following two very strong years), the funded ratios stood at roughly 79 percent for both ERS and TRS, and 88 percent for BERS.3 Lengthening the amortization schedule will delay the pension funds’ progress toward consistently achieving or staying close to (truly) 100 percent funded status.

So again, why do this? What’s the motivation? One or both of the following might have something to do with it:

Under a UFT-backed state law signed by Hochul two years ago, the city must begin to cap class sizes at ultimate levels of 20-25 students, depending on grade level. The Independent Budget Office has estimated that additional costs to the city of hiring added teachers (even as enrollment continues to decline) will ramp up from $53 million in FY 2026 to $546 million in FY 2028.

In a June 2018 deal with then-Mayor Bill de Blasio, the Municipal Labor Committee (MLC) agreed to produce $1.1 billion in cumulative healthcare savings from 2019 to 2021, and $600 million in annual recurring savings thereafter. To come up with that amount, the MLC—including reps of DC 37 and UFT, along with all the other major city unions—initially agreed to a plan that would have shifted their retirees to Medicaid Advantage accounts. But the retirees have fought off that plan in court, and UFT President Michael Mulgrew withdrew his support for it. The city, meanwhile, still wants the unions to deliver that $600 million a year in promised healthcare savings.

From a UFT perspective, the putative $11 billion reduction in pension contributions resulting from the amortization stretch-out over the next seven years would help cover the cost of the class size reduction. It could also help fill the budget hole created by the failure of all the major city unions to produce the promised $600 million a year in healthcare savings. And Lander’s budget hearing exchange with Brannan seemed to link the pension gambit with the need to fill the healthcare savings hole, especially if federal aid cuts soon materialize.

But at the end of the day, as the comptroller also noted, the proposed pension change will require present and future city taxpayers to foot the bill for “substantially more dollars in the out years than you see savings in the next decade.” The governor and the mayor need to publicly explain how this could be justified as anything more than a convenient way for unions to pay for concessions they’d rather not have to make.

Those figures are strictly illustrative, based (like all pension contribution projections) on the assumption that pension fund assets deliver the 7 percent return reflected in their liability discount rates. If, say, returns average less than 7 percent over the next few years, the initial savings will be less, and vice versa.

A screen-cap of the full message follows—note how the trustees are peeved up about “misinformation” being spread by nameless parties:

Those numbers are not as good as they look, because the “liability” side of the ratio is calculated using a generous 7 percent discount rate—a level Mike Bloomberg once compared to a promise from Bernie Madoff. The median assumed rate of return among multiemployer funds as of last week was 6.6 percent; the Common Retirement Fund of New York State discounts liabilities at a 5.9 percent rate; and the closest thing to a risk-free rate, the 30-year U.S. Treasury bill yield, is about 4.7 percent at this writing. In fiscal 2021, when the ERS, TRS, and BERS were reporting actuarial funded ratios of 93 percent, 100 percent, and 121 percent, respectively, the funded ratios calculated based on risk-free market interest rates were 55 percent, 58 percent, and 69 percent respectively, I estimated in this Empire Center report.

Irony: the reduction of the city pension funding over the term would be $600 million less a year 🤔. That is the same amount of money The unions were going to need to finance The health insurance premium stabilization fund for active workers with no oversight, that’s been used as a slush fund by both the municipal labor committee and mayors because the court blocked them from forcing retirees into a single Medicare advantage plan that many of their doctors in hospitals did not accept for treatment or payment.

First, they tried to charge Retirees full premium to stay on a federal public health benefit, if they refused to be forced into a Medicare advantage plan. Retirees were promised traditional Medicare would be their plan for 60 years. And remember Retirees are no longer in unions on retirement. And many are not in unions because they’re managerial

Then they tried to pass increasing co-pays and deductibles on Retirees again who were not part of any negotiation because they retired.

When the court stopped that too, they pulled the nuclear option attempted to kill all choices of healthcare plans for retirees and force them again into a single Medicare advantage plan that many of their doctors in hospitals would not accept

Since Retirees are no longer in the union, they weren’t at the table, they became the menu

Retirees don’t vote on contracts, they’re not part of negotiations, and they don’t vote for union officers

Egregious to even hear these words come from my mouth, but these failed union leaders thought it would be OK to steal vested healthcare benefits from retired civil servants, to finance their own raises and benefits. If they wanted a change in benefits they should have applied to themselves! Not people they cannot negotiate for under the law because they’re not in their union.

When that wasn’t successful, they decided to play a pension Ponzi scheme with pensions that would not only potentially have an impact on current Retirees, but future Retirees and taxpayers. And they never even told their members, active or retired.

The Uft then chose to attack us for revealing this very scheme. Some even said we were taking guidance from a right wing think tank. I guess they didn’t hear Brad Lander agree in the city council budget hearing 🤦🏽♀️

When traditionally opposing views agree, everyone should pause.

What do you know? When Mulgrew says jump, looks as though NYS government officials say how high?

How many pockets has Mulgrew stuck his hands into? First he gets himself $1.1B from the Stabilization Fund to hand out under the guise of retroactive raises, then he thinks no one will notice when he tries to throw 250,000 NYC municipal Medicare eligible retirees into a sub par Medicare Advantage plan without having researched in depth the ramifications of that. Then he pretends to no longer support the Medicare Advantage plan but doesn’t lift a finger to protect the retiree health benefits by backing their proposed legislation in the city council or writing an amicus brief. Nah he didn’t do that. Now he’s on the hook for the $600m he promised NYC yearly in perpetuity. What better place to get the money but from those who worked decades for NYC for a promised solvent defined pension benefit and healthcare? Why care about or respect anyone when he can get the NYS elected officials to do his bidding? Right the police and firefighter unions declined to participate in this scheme. This sure isn’t what a union is supposed to be but I guess Weingarten forgot to pass that information on to Mulgrew. Then again Sandra Feldman didn’t tell Weingarten.